.png)

.png)

Budgets are treated as a quarterly chore—a structured process on paper but disconnected from day-to-day financial decisions.

Finance teams consolidate numbers, assess department requests, and ensure spending aligns with approved budgets. Yet, despite following best practices, budgeting remains reactive rather than strategic. By the time actuals are compared against planned budgets, deviations have already occurred, making course correction difficult.

To build a budgeting system that drives business growth, organizations need more than just forecasts and approvals. They need real-time visibility, structured alignment, and a process that adapts to financial realities. Without this, budgets become rigid constraints rather than a tool for financial discipline and strategic decision-making.

In this blog post, we’ll explore how businesses can move beyond static budgets and create a dynamic financial system—one that not only keeps spending in check but also supports strategic decision-making and long-term growth.

Why Budgeting isn’t the Same for Every Organization

The way organizations allocate and track budgets depends on their size, structure, and operational complexity. It’s not just about handling larger revenue or expenses—it’s about how financial responsibilities are distributed.

Smaller businesses operate with fluid, activity-based budgeting. A single person or a small team handles multiple financial areas, from marketing spend to vendor payments. Rather than allocating budgets by department, they categorize expenses by key business activities, allowing flexibility as financial needs shift.

In contrast, medium and large enterprises follow a structured, department-based approach. Each function—IT, HR, sales, and operations—has a dedicated budget, with CFOs and department heads working together to align spending with business goals.

Industries like manufacturing take an even more granular approach, budgeting at a line-item level—tracking costs down to materials, production units, or equipment.

What remains constant across all businesses is that a budget cannot be treated as a theoretical exercise—simply setting financial targets at the beginning of the year isn’t enough. Budgets must be continuously monitored and adjusted in response to actual financial activity.

Most businesses treat budgeting as an isolated task—finance teams spend weeks crunching numbers, department heads submit requests, and a final document is approved. But as soon as actual spending begins, the budget gets sidelined.

The goal isn’t just to allocate funds; it’s to build a system where budgeting aligns with real-time financial activity and supports business growth.

When budgets and spending exist in separate silos, businesses risk operating on outdated assumptions, leading to misallocated resources, inefficient cash flow management, and difficulty in meeting long-term goals.

Here’s how to prepare a budget for a company effectively.

Step 1: Analyze Last Year’s Budget—What Worked, What Didn’t?

Before planning for the next cycle, finance teams need to evaluate how last year’s budget played out. This isn’t just about comparing planned vs. actual figures but also about understanding why those deviations happened.

Here’s how to extract meaningful insights from past budgets:

- Identify major variances – Where did actual spending exceed or fall short of projections? Were certain costs underestimated or overestimated?

- Find the root cause – Was overspending due to rising supplier costs, unexpected hiring, or poor forecasting? Were some budgets too conservative, leaving growth opportunities untapped?

- Check revenue assumptions – Were revenue projections too optimistic or too cautious? If revenue exceeded expectations, did budget allocations reflect that, or did teams continue operating within old constraints?

So if marketing was allocated $500K but ended up spending $700K due to higher-than-expected customer acquisition costs, the question isn’t just about increasing the marketing budget—it’s about re-evaluating assumptions.

Was the return on ad spend (ROAS) worth it? Did the company underestimate the competition?

By thoroughly analyzing past budgets, finance teams don’t just carry forward last year’s numbers—they create a budget that reflects business realities and aligns financial planning with actual performance.

Step 2: Revenue Planning—How Much Do You Expect to Earn?

Budgeting isn’t just about cost control—it should start with revenue. The first question should always be: Where is our money coming from next year?

For large enterprises, revenue planning involves:

- Sales forecasts— Estimates based on pipelines, existing customer contracts, and market trends.

- Scenario planning—What happens if the economy slows? What’s the minimum revenue needed to sustain operations?

For SMEs and startups, it’s about:

- Identifying core revenue streams—Which products/services bring the most consistent income?

- Evaluating pricing models—Should you increase prices or add premium services?

- Understanding seasonality—Do you need a lean budget in slower months?

This isn’t just about forecasting sales—it’s about ensuring budget allocations align with the business's growth plan. If revenue projections are off, budgets will either constrain growth (by being too conservative) or cause overruns (by overestimating resources).

Step 3: Expense Planning—Where Will the Money Go?

Once revenue projections are set, the next step is distributing that income strategically. The starting point is deciding how to divide budgets—whether by department, function, project, or revenue stream.

To ensure consistency, each expense category should be mapped to the same GL codes used in accounting and financial reporting. This makes tracking spending against the budget easier in real time without manual reconciliation.

The structure depends on how the business operates, but the key is to ensure that budget categories align with how actual expenses are recorded and tracked.

Collaboration between finance and department heads

Budgeting isn’t just a finance team’s job. For it to work, department heads need to be actively involved.

Finance teams should guide each department through:

- Understanding their historical spending – What was spent last year? Were there overruns? Did we allocate too much to a low-impact initiative?

- Setting forward-looking goals – What are their priorities for the next year? Do they need more resources? Are there cost-saving opportunities?

- Defining constraints and trade-offs – If revenue is growing by 10%, should hiring increase at the same rate? Or should we optimize existing teams?

- Ensuring budgets reflect real business needs – Rather than taking a top-down approach, finance should act as a strategic advisor, helping each department build budgets that align with both financial discipline and growth strategy.

Instead of blindly cutting expenses, finance teams should analyze constraints and levers. By making expense planning a collaborative, data-driven process, finance teams ensure that budgets are not just spending limits but strategic tools for business growth.

Step 4: Choosing the Right Budgeting Method

The best budgeting method depends on your company’s size, structure, financial priorities, and how predictable your revenue and expenses are. Each method has its advantages, but choosing the right one requires understanding when and why to apply it.

1. Zero-Based Budgeting (ZBB) – Best for Cost Control & Dynamic Businesses

Instead of rolling over last year’s budget, every expense is justified from scratch. This approach forces teams to prioritize spending based on actual business needs rather than habit.

When to use:

- Companies undergoing financial restructuring or looking for aggressive cost control

- Businesses with volatile revenue that require frequent budget adjustments

- Organizations launching new products or entering new markets where past spending data is irrelevant

Example: A mid-sized SaaS company looking to optimize costs after a funding round may use ZBB to reassess every software subscription, contractor expense, and marketing campaign—eliminating anything that doesn’t contribute to revenue.

2. Incremental Budgeting – Best for Stable, Established Companies

Here, last year’s budget is used as a baseline, with small percentage increases or decreases based on expected growth or cost changes. However, this method assumes past spending patterns are always relevant, which leads to inefficiencies if outdated expenses are never reevaluated.

When to use:

- Organizations with predictable revenue and expenses, like mature enterprises

- Companies with well-structured departmental budgets that only require minor adjustments

- Businesses where historical spending is a reliable indicator of future needs

Example: A large manufacturing firm with steady production costs and long-term supplier contracts uses incremental budgeting to adjust for inflation and raw material price fluctuations.

3. Activity-Based Budgeting (ABB) – Best for Performance-Driven Planning

Instead of allocating budgets by department, ABB assigns costs based on specific activities or business processes. However, it requires detailed cost tracking and is harder to implement without real-time financial visibility.

When to use:

- Companies looking to link spending directly to business outcomes

- Industries with high operational costs, like manufacturing and logistics

- Growing companies that need to allocate resources based on output rather than departments

Example: A logistics company forecasting 10,000 additional shipments next quarter budget based on the cost per shipment rather than assigning a fixed amount to the operations department.

Which Budgeting Method Should You Use?

Most companies don’t rely on just one approach—they often combine methods based on their needs.

- A startup expanding rapidly? → Use ZBB to reallocate resources dynamically.

- A large enterprise with predictable costs? → Use incremental budgeting with periodic reviews.

- A business scaling production? → Use ABB to tie costs directly to growth.

The key is ensuring your budgeting method supports financial visibility and decision-making rather than just being an administrative task.

Step 5: Align Budgeting With Real-Time Spending

The most common budgeting failures stem from the disconnect between planned budgets and real-world spending behavior.

- Spending happens first, reconciliation happens later: Expenses accumulate throughout the month, but they’re only checked against budgets at period-end, leaving no room for adjustments.

- Budgets and actuals don’t align: Many companies create budgets in spreadsheets or separate tools, while actual expenses are recorded in ERPs or accounting systems with different categorizations, business codes, or GL structures. This mismatch makes real-time tracking difficult.

- Lack of visibility: Budget owners don't have immediate access to updated spending data, making it impossible to course-correct before exceeding limits.

- Manual reconciliation is time-consuming and error-prone: Finance teams export data from ERPs, compare it against budgets, and identify deviations manually— slowing down decision-making.

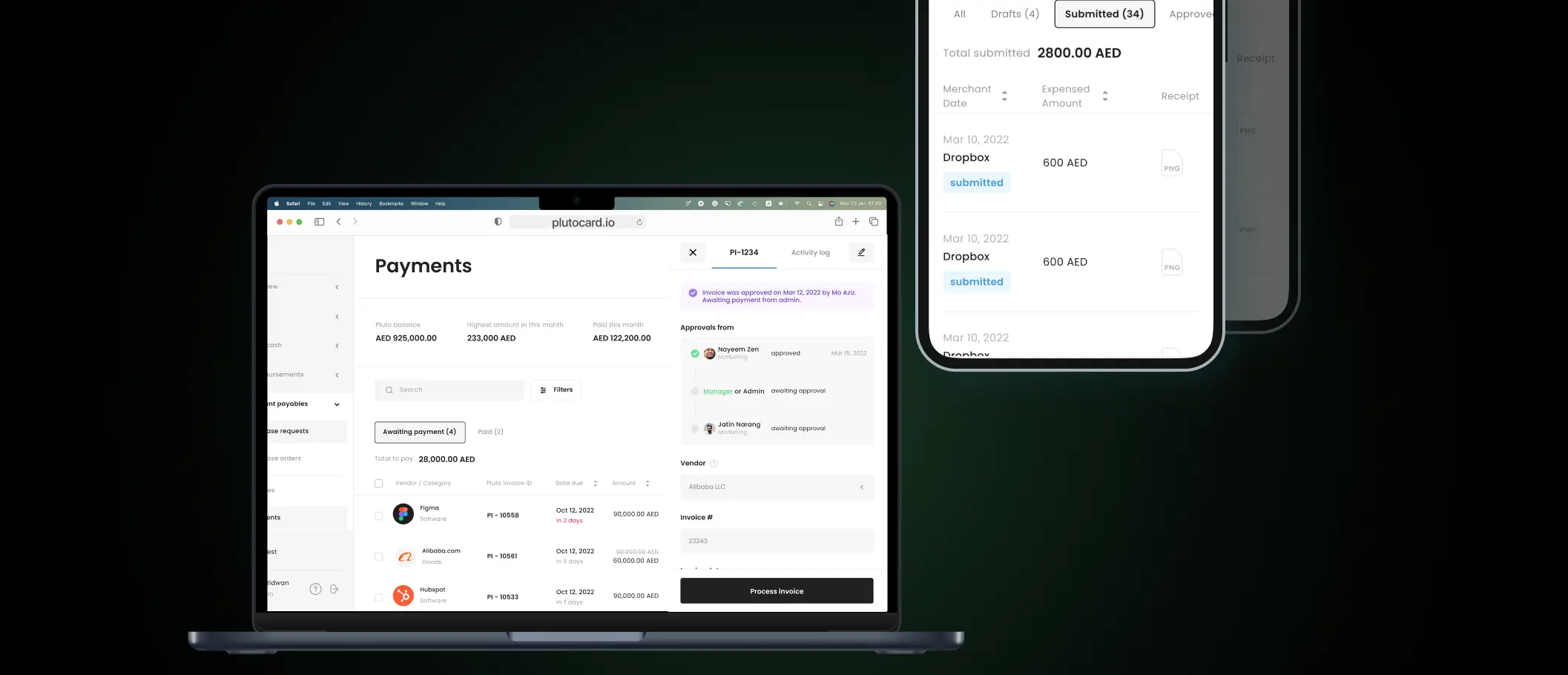

Integrating Budgeting & Spend Management in a Unified System

Instead of treating budgeting and spend tracking as separate functions, businesses need a single system where both are aligned in real-time.

A unified system integrates budgeting, spend management, and accounting in real time. Instead of waiting until the end of the month to compare budget vs. actuals, every expense is logged immediately, categorized under the right department or cost center, and mapped against the budget.

This allows finance teams to:

- Catch deviations before they escalate – Instead of discovering budget overages at quarter-end, teams intervene early and reallocate funds strategically.

- Ensure budgets remain realistic and actionable – When spending is continuously updated, finance teams adapt budgets dynamically rather than working with outdated assumptions.

- Reduce manual reconciliation and improve accuracy – Since budgets and actuals use the same GL structure and departmental coding, data discrepancies are minimized, and reporting is streamlined.

Budgeting should not be a disconnected, back-office process. When integrated with real-time spend tracking, it becomes a powerful financial control tool that helps businesses scale confidently.

Unifying Budgets and Spending for Real-Time Control

A well-structured budget is only as effective as the spending discipline that follows. Without a system that ensures budgets are actively tracked and followed through, finance teams are left reconciling expenses after the fact—often when it’s too late to prevent overspending.

Budget compliance isn’t just about limiting costs; it’s about strategically allocating every dollar, giving teams the clarity they need to operate within financial constraints while still achieving business goals.

Pluto brings budgeting, spend management, and accounting together—so finance teams control costs, improve forecasting, and align financial decisions with strategic goals.

Finance teams get real-time visibility, reducing surprises and enabling proactive adjustments. Instead of waiting for month-end reports, they track variances instantly, ensure compliance, and make informed financial decisions without manual intervention.

Book a demo to see how Pluto transforms budgeting into a continuous, data-driven process.